Prompt overview

-

Analyzes income, filing status, deductions, and life events to find legal, often‑missed tax savings.

-

Ranks actions by impact and ease, with rough dollar estimates and required documentation.

-

Covers both this year’s quick wins and next year’s planning moves.

Quick Specs

- Media: Text

- Use case: Analysis, Content Strategy, Enhancement

- Industry: Tax Services

- Techniques: Plan-Then-Solve, Role/Persona Prompting, Structured Output

- Models: Claude 3.5 Sonnet, Gemini 2.0 Flash, GPT-4o, Llama 3.1 70B

- Estimated time: 15-30 minutes

- Skill level: Advanced

Variables to fill

-

Annual income and sources: {income_sources}

-

Employment type/status (W‑2, self‑employed, contractor, mixed): {employment}

-

Filing status (single/MFJ/HOH/etc.): {filing}

-

Current deductions and expenses (mortgage interest, SALT, charity, medical, education, childcare, HSA, etc.): {deductions}

-

Financial goals and major life changes (marriage, move, baby, home, education, job change): {goals_changes}

Example variables block (copy and edit)

-

{income_sources}: $145k W‑2 salary + $8k freelance + $3k interest/dividends

-

{employment}: W‑2 with side gig (Schedule C)

-

{filing}: Married filing jointly

-

{deductions}: mortgage interest $11k; SALT $7k; charity $2.5k; HSA $2k; childcare $7k; student loan interest $900

-

{goals_changes}: new baby, plan to buy a home upgrade next year

Prompt template

Act as an expert US tax strategist and CPA focused on maximizing legal tax savings for individuals across income levels and employment types. Build a personalized, prioritized plan with clear steps, estimated savings, and documentation notes. Use a US context and current federal rules; flag items that commonly vary by state.

Inputs

– Income and sources: [income_sources]

– Employment type/status: [employment]

– Filing status: [filing]

– Current deductions/expenses: [deductions]

– Financial goals and major life changes: [goals_changes]

Process

1. Profile snapshot: summarize income mix, filing status, and likely credit/deduction lanes (standard vs. itemize, above‑the‑line deductions, credits).

2. Opportunity scan: evaluate common and advanced areas—retirement contributions (401(k)/403(b)/IRA/SEP/Solo 401(k)), HSA/FSA/DC FSA, child/dependent credits, education credits, QBI for self‑employed, charitable strategies (bunching/DAF), mortgage/SALT caps, energy‑efficient home/vehicle credits, loss harvesting, timing shifts, and withholding/estimated tax alignment.

3. Estimate savings: provide rough federal savings using marginal tax rate bands; note state impact where typical.

4. Prioritize: classify each action as High, Medium, or Low Impact based on potential savings and ease/eligibility.

5. Documentation: list exactly what records or forms are needed for each item.

6. Planning forward: include moves for next year that require setup now (e.g., Solo 401(k), W‑4 changes, quarterly estimates, DAF).

Output format (return this only)

A) Heading: Profile Summary (Plain English)

– One short paragraph restating [employment], [filing], main income sources, and whether standard deduction or itemizing is likely this year.

B) Heading: High Impact (Do These First)

– 5–8 bullets. Each bullet must include: Action | Est. federal savings (USD) | Why it applies | Documentation needed.

Examples to consider as applicable:

– Max traditional 401(k)/403(b)/457 or pre‑tax deferrals; backdoor Roth steps if eligible.

– HSA contributions up to annual limit (if HDHP).

– Child/Dependent Care Credit or Dependent Care FSA coordination.

– SEP‑IRA or Solo 401(k) for self‑employment income (deadline notes).

– QBI deduction optimization for qualified business income (entity/threshold considerations).

– Charitable bunching via Donor‑Advised Fund when near itemization threshold.

C) Heading: Medium Impact (Good Next)

– 5–8 bullets in the same Action | Est. savings | Why | Docs format.

Examples: student loan interest deduction (AGI limits), American Opportunity/Lifetime Learning Credits, energy‑efficient home and EV credits, tax‑loss harvesting in brokerage, shifting income/expenses across year‑end within rules, accountable plan for employee reimbursements (if applicable), spousal IRA.

D) Heading: Low Impact (Nice to Have)

– 4–6 bullets with smaller but legitimate savings (e.g., educator expenses if eligible, small business home office simplified method, subscription/professional dues, job‑related education where allowed, clean recordkeeping to avoid missed credits).

E) Heading: Itemized vs. Standard Deduction Check

Provide a small markdown table comparing this year’s likely totals:

Category | Estimated Amount (USD) | Notes

Rows: Standard Deduction (by [filing]), Mortgage Interest, SALT (capped as applicable), Charitable, Medical (over AGI threshold), Other.

– Conclude with “Likely better to [itemize/claim standard] this year” based on the totals provided.

F) Heading: Withholding and Quarterly Estimates

– Bullets on adjusting W‑4 or making estimated payments to avoid underpayment penalties (safe harbor rules), including due dates (Apr 15, Jun 15, Sep 15, Jan 15).

– Simple rule: align withholding/estimates to 100% of last year’s tax (110% if prior AGI > $150k) or current‑year projection.

G) Heading: Documentation Checklist (What to Gather)

– Income: W‑2s, 1099‑NEC/1099‑K/1099‑INT/1099‑DIV/1099‑B.

– Deductions: mortgage interest Form 1098, property tax statements, charity receipts (contemporaneous), tuition Form 1098‑T, student loan 1098‑E, medical EOBs.

– Business (if any): ledger, receipts, mileage log, home office worksheet, 1099s sent.

– Retirement/HSA: year‑end statements, Form 5498/5498‑SA, plan confirmations.

– Energy/EV: manufacturer certificates, invoices, placed‑in‑service dates.

H) Heading: Planning Moves for Next Year

– 4–8 bullets: open/adjust Solo 401(k) or SEP timing, consider Roth conversions in low‑income years, harvest gains within 0% bracket if eligible, bunch charity with DAF, review insurance and FSA elections, shift RSU sale timing, optimize ESPP disqualifying vs. qualifying dispositions, update W‑4 after life events.

I) Heading: Assumptions and Caveats

– Dollar estimates use federal marginal brackets and do not include state taxes unless specified.

– Credits and limits phase out at higher AGIs; confirm eligibility.

– Educational; not tax or legal advice.

Rules

– Keep language simple and specific; no hype.

– Use USD formatting and round savings to the nearest $50 where appropriate.

– If an input is missing, ask one concise clarifying question at the top, then proceed with clearly labeled assumptions.

– Do not request or process sensitive identifiers.

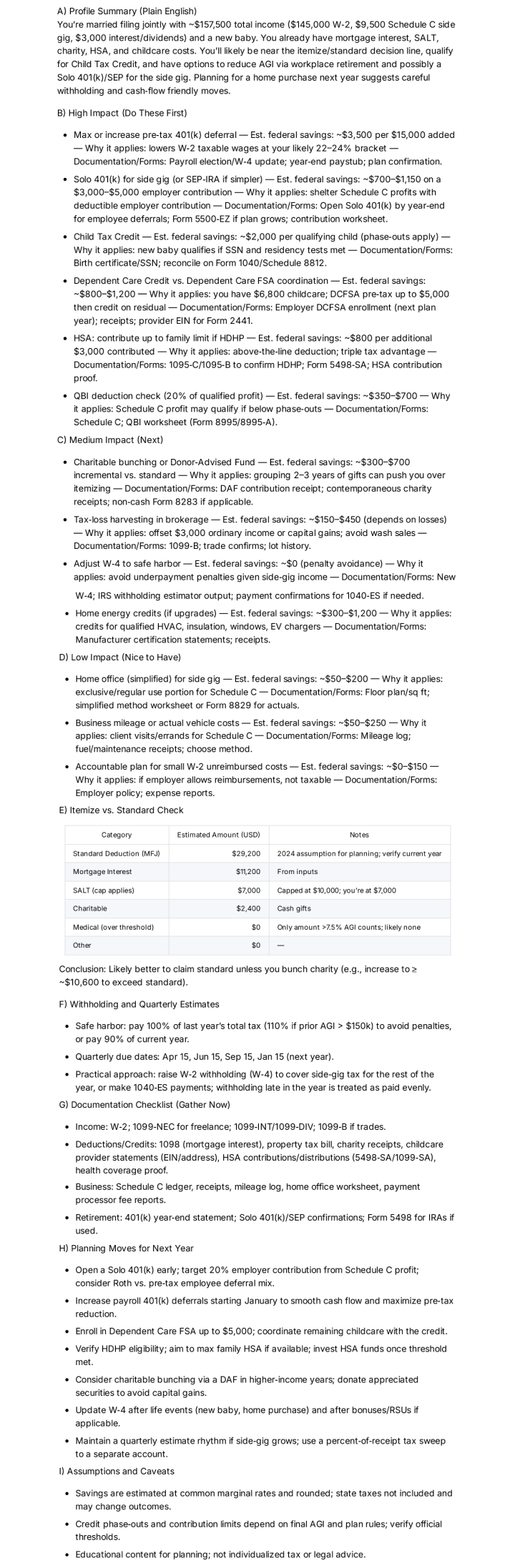

Sample Output

How to use

-

Fill the variables with income mix, filing status, deductions, and goals.

-

Run the prompt; complete High Impact items first, then Medium, then Low.

-

Save documentation as PDFs and keep a checklist for each item.

-

Re‑run after major life changes or before year‑end to update projections.

FAQ

-

Standard vs. itemize—how to decide?

Compare itemizable totals to the standard deduction for {filing}; choose the larger to reduce taxable income. -

Traditional vs. Roth contributions?

Use marginal‑rate now vs. expected future rate; traditional cuts current taxes, Roth favors future tax‑free growth. -

What if there’s side‑gig income?

Consider SEP or Solo 401(k), QBI eligibility, and quarterly estimates to avoid penalties.

Compliance and notes

-

Educational template only; not individualized tax, legal, or accounting advice. Rules can change; verify eligibility.

-

Do not paste Social Security numbers or full account numbers.

Revision history

-

v1.1 – Added impact tiers with doc requirements and itemize vs. standard comparison – 2025‑10‑13