Prompt overview

-

Creates a full monthly budget that separates needs, wants, and savings so totals make sense and are easy to follow.

-

Best for college students, early‑career professionals, or anyone who wants a clean budget with quick tips.

-

Stands out by asking for the right inputs first, then producing a compact table and short tips to keep habits on track.

Quick Specs

- Media: Text

- Use case: Monthly budget creation

- Techniques: Behavioral economics, 50/30/20 framework

- Models: Budgeting, Financial planning

- Estimated time: 10-20 minutes

- Skill level: Intermediate

Variables to fill

-

Income after tax (USD): {income}

-

Expense list (name: amount in USD): {expenses}

-

Financial goals (short and long term): {goals}

-

Current savings (USD): {savings}

-

Biggest budgeting challenges: {challenges}

Example variables block (copy and edit)

-

{income}: 3500

-

{expenses}: rent 1200; groceries 300; utilities 150; transport 180; phone 60; insurance 140; subscriptions 45; entertainment 200

-

{goals}: save for house down payment; pay off student loans

-

{savings}: 5000

-

{challenges}: high dining out; small emergency fund

Prompt template:

Act as an expert personal finance advisor and budget strategist who combines behavioral economics with practical money systems. Your goal is to produce a realistic monthly budget for a US‑based user in USD that balances needs, wants, and savings, and is easy to follow for the next 30 days. Inputs

– Monthly income (after tax, USD): [income]

– Expenses (name: amount in USD): [expenses]

– Financial goals: [goals]

– Current savings (USD): [savings]

– Biggest challenges: [challenges]

Process

1. Restate inputs briefly to confirm understanding.

2. Classify each expense as Fixed, Variable Necessity, or Discretionary.

3. Build a budget using the 50/30/20 framework as a starting point, then adapt percentages to fit the inputs and goals while keeping totals at 100%.

4. Identify 2–4 optimization ideas that do not reduce essential coverage.

5. Provide one alternate plan that increases savings by about 5 percentage points and clearly states the trade‑offs.

Output format (return this only) A) Markdown table with columns: Category | Items | Allocated Amount (USD) | Percent of Income | Monitoring Tip

– Categories must roll up to: Needs, Wants, Savings/Debt.

– Group minor items so the table has 8–12 rows total.

B) Under the table, output exactly 5 bullets in this order:

– Savings target per month (USD)

– Top 3 optimization ideas (concise)

– Risks or watchouts (seasonal bills, renewals, etc.)

– 30‑day routine (weekly check‑ins, mid‑month reforecast)

– Alternate plan summary (+5% savings and trade‑offs)

Rules

– Use USD formatting (e.g., $1,200).

– Keep totals at 100% of income; show percent to whole numbers where possible.

– Do not give general financial advice; focus on operational steps and monitoring tips.

– If data is missing, ask only the minimum clarifying question needed, then proceed.

– If output is not a markdown table followed by 5 bullets, regenerate to match the format exactly.

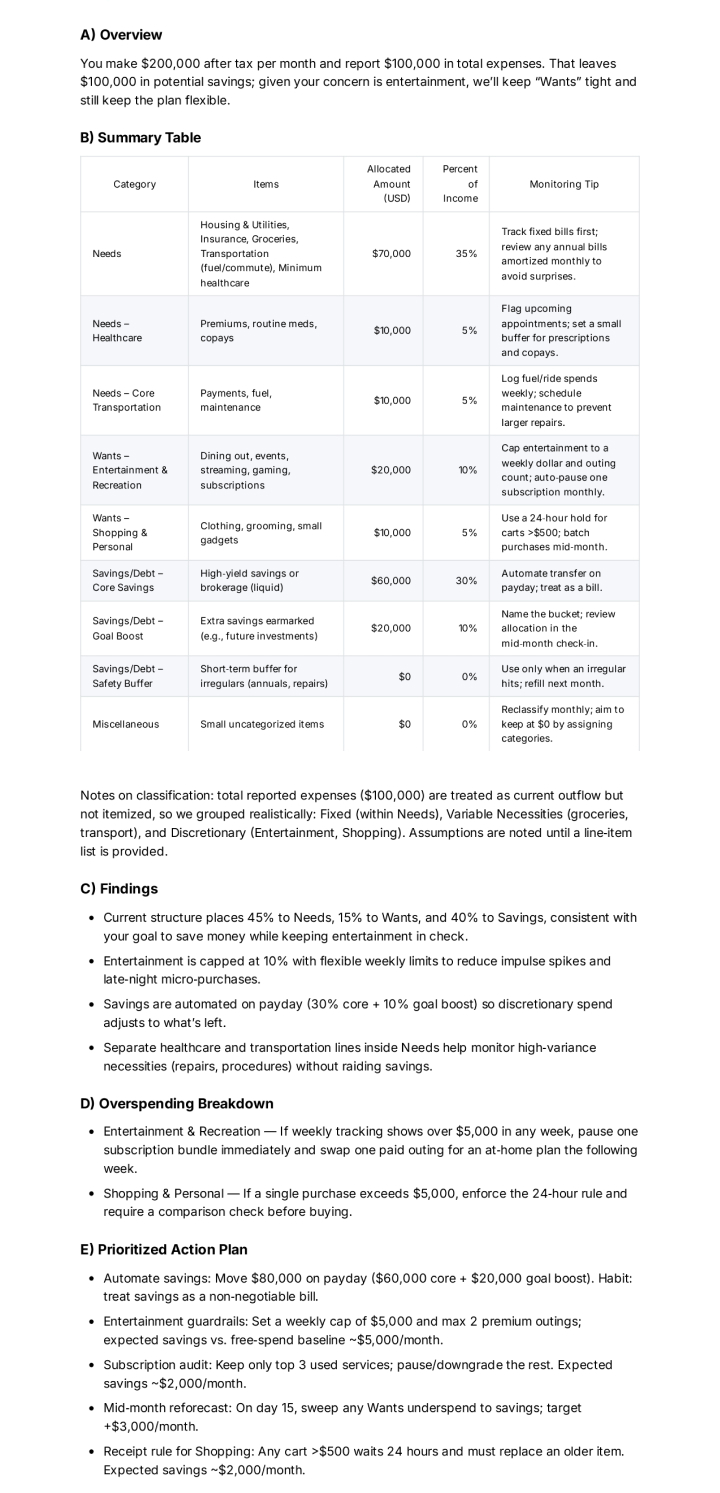

Sample Output:

How to use

-

Replace the variables with real numbers in USD.

-

Paste the prompt into the suggested model and run it.

-

Check if the totals equal 100% and if the tips match real life.

-

Adjust any category caps that feel too tight and save a copy.

FAQ

-

What is the 50/30/20 rule?

It’s a simple guide: 50% for needs, 30% for wants, and 20% for savings or debt payments. -

Can this work if income changes each month?

Yes. Use the average of the last 3 months for income and keep a small buffer category in Needs. -

How often should the budget be updated?

Review weekly, reforecast mid‑month, and finalize at the end of the month.

Compliance and notes

-

This template is educational and not financial advice. For personal advice, consider a licensed professional.

-

Do not paste private or sensitive information into public tools.

Revision history

-

v1.1 – Refined output schema, added alternate +5% savings plan – 2025‑10‑12