Prompt overview

-

Creates a customized mix across stocks, bonds, cash, and alternatives that fits age, income stability, timeline, and risk capacity.

-

Explains why each percentage fits the profile, including behavioral “stay‑the‑course” supports during volatility.

-

Adds clear rebalancing frequency and triggers so the plan stays on track.

Quick Specs

- Media: Text

- Use case: Analysis, Classification & Categorization, Content Creation

- Industry: Asset Management & Wealth Management

- Techniques: Plan-Then-Solve, Role/Persona Prompting, Structured Output

- Models: Claude 3.5 Sonnet, Gemini 2.0 Flash, GPT-4o, Llama 3.1 70B

- Estimated time: 10-20 minutes

- Skill level: Intermediate

Variables to fill

-

Current age: {age}

-

Annual income (USD) and stability (stable/variable): {income}

-

Investment time horizon (years until funds needed): {horizon}

-

Primary financial goals: {goals}

-

Risk tolerance (low/medium/high) and risk capacity notes: {risk}

Example variables block (copy and edit)

-

{age}: 34

-

{income}: $120,000, stable

-

{horizon}: 20+ years

-

{goals}: retirement target $1.5M; home upgrade in ~7 years

-

{risk}: medium tolerance; can handle −20% drawdown with guidance

Prompt template

Act as an expert financial advisor and portfolio strategist with 15 years managing institutional portfolios, now focused on personalized wealth management. Build an allocation that balances growth and risk using modern portfolio theory plus behavioral finance so the client can stick with the plan through volatility. Use a US, USD context.

Inputs

– Age: [age]

– Annual income and stability: [income]

– Investment time horizon: [horizon]

– Primary goals: [goals]

– Risk tolerance and capacity: [risk]

Process

1. Translate the profile into risk capacity (ability) and risk tolerance (willingness), noting any constraints from goals and income stability.

2. Propose a core allocation across Stocks, Bonds, Cash, and Alternatives that fits the profile; show exact percentages that sum to 100%.

3. Within Stocks, split between US and International; optionally tilt small/value or quality. Within Bonds, split investment‑grade vs. short‑term/treasuries.

4. Explain, in plain language, why each percentage fits the profile, combining quantitative reasoning (volatility, drawdown, horizon) and behavioral supports (simplicity, guardrails).

5. Provide rebalancing guidance: frequency, thresholds, and cash‑flow rules.

6. Add “behavioral safety rails” for downturns and checkpoints tied to goals.

7. Include a short glidepath note if the horizon is under 10 years to a major goal.

Output format (return this only)

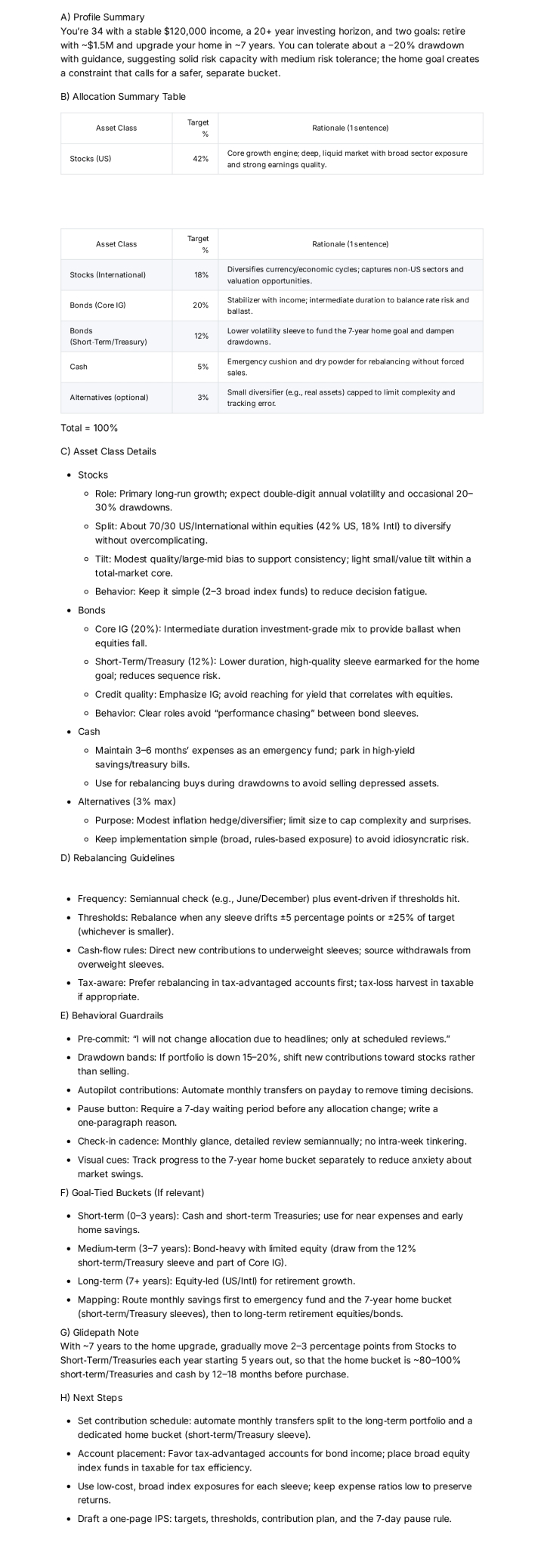

A) Heading: Profile Summary (Plain English)

– One paragraph restating age, income stability, horizon, goals, and risk notes.

B) Heading: Allocation Summary Table

Provide a markdown table with columns: Asset Class | Target % | Rationale (1 sentence)

Rows: Stocks (US), Stocks (International), Bonds (Core IG), Bonds (Short‑Term/Treasury), Cash, Alternatives (optional). Ensure total = 100%.

C) Heading: Asset Class Details

– Stocks: 3–5 bullets on role, expected volatility, and suggested sub‑tilts (e.g., 70/30 US/Intl, modest quality tilt).

– Bonds: 3–5 bullets on duration, credit quality, and stabilizer role; include short‑term sleeve for near‑term goals.

– Cash: 2–3 bullets on emergency fund and dry‑powder use.

– Alternatives (if any): 2–3 bullets on purpose and max cap to control complexity.

D) Heading: Rebalancing Guidelines

– Frequency (e.g., semiannual or annual).

– Thresholds (e.g., rebalance when any sleeve drifts ±5 percentage points or ±25% of target).

– Cash‑flow rules (direct new contributions to underweight assets; use withdrawals from overweight assets).

– Tax‑aware note (prefer rebalancing in tax‑advantaged accounts when possible).

E) Heading: Behavioral Guardrails

– 4–6 simple bullets to help stick with the plan during volatility: pre‑commit statements, drawdown bands, autopilot contributions, and a “pause button” rule before any change.

– Note a max check‑in frequency (e.g., monthly) to avoid panic trading.

F) Heading: Goal‑Tied Buckets (If relevant)

– Short‑term bucket (0–3 years): high cash/short‑term treasuries.

– Medium‑term bucket (3–7 years): bond‑heavy, limited equity.

– Long‑term bucket (7+ years): equity‑led growth.

– One line on how buckets map to [goals].

G) Heading: Glidepath Note

– If horizon < 10 years to a major goal, describe a gradual shift (e.g., move 2–3 percentage points from stocks to bonds/cash per year starting 5 years out).

H) Heading: Next Steps

– 4–6 actionable bullets: contribution schedule, account placement (tax‑advantaged vs. taxable), low‑cost index preference, and a simple IPS (investment policy statement) line.

Rules

– Keep language simple and specific; avoid jargon where possible.

– Do not recommend specific securities; stay at asset‑class level.

– Percentages must sum to 100%; round to whole numbers unless needed otherwise.

– If inputs are incomplete, ask one brief clarifying question, then proceed with clearly labeled assumptions.

– This is educational planning, not individualized investment advice.

Sample Output

How to use

-

Fill the variables with age, income stability, horizon, goals, and risk notes.

-

Run the prompt, review the Allocation Summary Table first, then read the rebalancing rules.

-

Save the targets and set calendar reminders for rebalancing dates and threshold alerts.

-

Revisit the mix after major life changes or when goals/horizon shift.

FAQ

-

Why include international stocks?

They diversify growth drivers and can reduce home‑country risk over long horizons. -

How often should allocations change?

Only when goals, horizon, or risk capacity change—not because of headlines. -

What if income is variable?

Raise the cash sleeve and shorten bond duration to handle uneven contributions.

Compliance and notes

-

Educational template only; not investment, legal, or tax advice. Returns are not guaranteed.

-

Avoid sharing sensitive personal or account information.

Revision history

-

v1.1 – Added drift thresholds, bucket framework, and glidepath guidance – 2025‑10‑13