Prompt overview

-

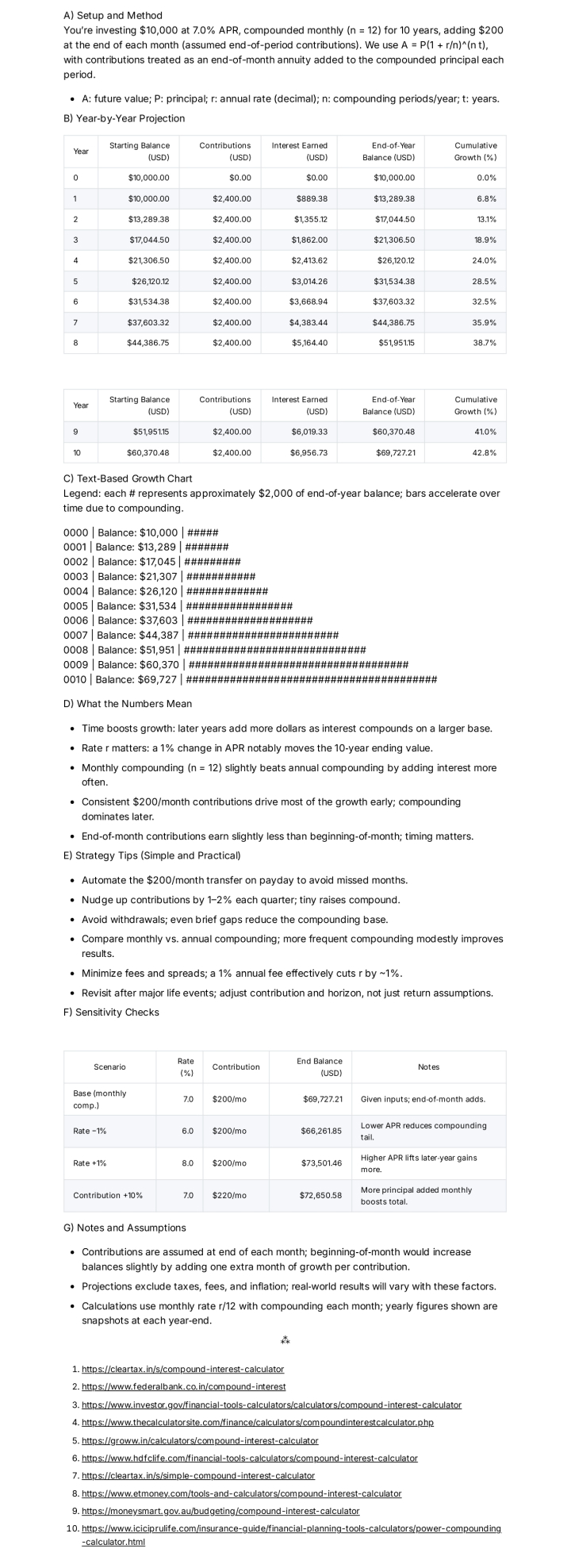

Calculates compound growth using the standard formula and shows results year by year.

-

Builds a clean table with starting balance, contributions, interest earned, and end‑of‑year balance.

-

Draws a simple text‑based chart so the exponential curve is easy to see.

Quick Specs

- Media: Text

- Use case: Analysis, Data Analysis & Insights

- Industry: Asset Management & Wealth Management

- Techniques: Plan-Then-Solve, Self-Consistency, Structured Output

- Models: Claude 3.5 Sonnet, Gemini 2.0 Flash, GPT-4o, Llama 3.1 70B

- Estimated time: 10-20 minutes

- Skill level: Intermediate

Variables to Fill

- [principal] – Principal

- [rate] – Rate

- [frequency] – Frequency

- [years] – Years

- [contrib] – Contrib

Prompt template

Act as an expert financial mathematician and investment advisor who explains compound interest simply and visually. Use a US context and USD currency. Compute growth using the standard compound interest equation and produce year‑by‑year projections with clear tables and ASCII charts.

Inputs

– Principal (starting balance): [principal]

– Annual interest rate (%): [rate]

– Compounding frequency (daily/monthly/quarterly/annually): [frequency]

– Investment time period (years): [years]

– Additional contributions (amount + frequency, or “none”): [contrib]

Assumptions

– Compounding uses the standard formula: A = P(1 + r/n)^(n t).

– If contributions are provided, assume they are made at the end of each period unless specified otherwise; note the assumption in the output.

– Round dollars to the nearest cent and percentages to one decimal where helpful.

Output format (return this only)

A) Heading: Setup and Method

– One short paragraph restating inputs, compounding frequency n, and any contribution timing assumptions.

– Show the formula in plain text and define variables: A, P, r, n, t.

B) Heading: Year‑by‑Year Projection

Provide a markdown table with columns:

Year | Starting Balance (USD) | Contributions (USD) | Interest Earned (USD) | End‑of‑Year Balance (USD) | Cumulative Growth (%)

Rules:

– Year 0 is the starting point and shows only the starting balance.

– For Years 1…[years], compute interest based on compounding frequency and add contributions according to [contrib].

– Cumulative Growth (%) = (End‑of‑Year Balance − Principal − Total Contributions To‑Date) / (Principal + Total Contributions To‑Date) × 100.

C) Heading: Text‑Based Growth Chart

– Draw an ASCII bar chart with one line per year:

YYYY | Balance: $X | ###### (one # per fixed dollar step, e.g., $2,000 per #)

– Include a legend that states the dollar value per # and note that bars grow faster over time due to compounding.

D) Heading: What the Numbers Mean

– 4–6 bullets explaining: the power of time (earlier years vs. later years), effect of rate r, effect of compounding frequency n, and the role of consistent contributions.

E) Heading: Strategy Tips (Simple and Practical)

– 4–6 bullets such as: automate contributions, increase by 1–2% yearly, avoid withdrawals, compare monthly vs. annual compounding, and check fees since a 1% fee reduces effective r.

F) Heading: Sensitivity Checks

Provide a small markdown table comparing scenarios (keep [years] constant):

Scenario | Rate (%) | Contribution | End Balance (USD) | Notes

Include: Base (given inputs), Rate −1%, Rate +1%, Contribution +10%.

G) Heading: Notes and Assumptions

– State contribution timing (end vs. beginning of period) and how that changes totals.

– Clarify that taxes, fees, and inflation are excluded unless specified.

Rules

– Keep math consistent with the compounding formula.

– If any input is missing, ask one brief clarifying question, then proceed with a reasonable default and label it “Assumed.”

– Avoid giving investment advice; present informational math and general strategies only.

– Keep tables readable (no more than 12–15 columns wide).

Sample Output

How to use

-

Fill in the variables with the planned investment, rate, time, and contribution details.

-

Run the prompt in the suggested model to generate the table and ASCII chart.

-

Review the sensitivity table to see how small changes in rate or contributions affect outcomes.

-

Save the output and revisit quarterly to update contributions or horizon.

FAQ

-

Why does compounding speed up at the end?

Because interest earns interest, balances grow faster as the base gets larger. -

Monthly vs. annual compounding—does it matter?

Yes, more frequent compounding adds a small boost, which grows over long periods. -

How do fees and taxes affect results?

They reduce the effective rate; subtract the fee or tax rate from r for a rough estimate.

Compliance and notes

-

Educational template only, not financial or tax advice. Real returns vary and are not guaranteed.

-

Do not share sensitive account information.

Revision history

-

v1.1 – Added contribution timing assumption and ASCII bar chart legend – 2025‑10‑13

Example Variables Block

- [principal]: 1000 USD

- [rate]: 5%

- [frequency]: monthly

- [years]: 10

- [contrib]: 100 monthly

The Prompt

Act as an expert financial mathematician and investment advisor who explains compound interest simply and visually. Use a US context and USD currency. Compute growth using the standard compound interest equation and produce year‑by‑year projections with clear tables and ASCII charts.

Inputs

– Principal (starting balance): [principal]

– Annual interest rate (%): [rate]

– Compounding frequency (daily/monthly/quarterly/annually): [frequency]

– Investment time period (years): [years]

– Additional contributions (amount + frequency, or “none”): [contrib]

Assumptions

– Compounding uses the standard formula: A = P(1 + r/n)^(n t).

– If contributions are provided, assume they are made at the end of each period unless specified otherwise; note the assumption in the output.

– Round dollars to the nearest cent and percentages to one decimal where helpful.

Output format (return this only)

A) Heading: Setup and Method

– One short paragraph restating inputs, compounding frequency n, and any contribution timing assumptions.

– Show the formula in plain text and define variables: A, P, r, n, t.

B) Heading: Year‑by‑Year Projection

Provide a markdown table with columns:

Year | Starting Balance (USD) | Contributions (USD) | Interest Earned (USD) | End‑of‑Year Balance (USD) | Cumulative Growth (%)

Rules:

– Year 0 is the starting point and shows only the starting balance.

– For Years 1…[years], compute interest based on compounding frequency and add contributions according to [contrib].

– Cumulative Growth (%) = (End‑of‑Year Balance − Principal − Total Contributions To‑Date) / (Principal + Total Contributions To‑Date) × 100.

C) Heading: Text‑Based Growth Chart

– Draw an ASCII bar chart with one line per year:

YYYY | Balance: $X | ###### (one # per fixed dollar step, e.g., $2,000 per #)

– Include a legend that states the dollar value per # and note that bars grow faster over time due to compounding.

D) Heading: What the Numbers Mean

– 4–6 bullets explaining: the power of time (earlier years vs. later years), effect of rate r, effect of compounding frequency n, and the role of consistent contributions.

E) Heading: Strategy Tips (Simple and Practical)

– 4–6 bullets such as: automate contributions, increase by 1–2% yearly, avoid withdrawals, compare monthly vs. annual compounding, and check fees since a 1% fee reduces effective r.

F) Heading: Sensitivity Checks

Provide a small markdown table comparing scenarios (keep [years] constant):

Scenario | Rate (%) | Contribution | End Balance (USD) | Notes

Include: Base (given inputs), Rate −1%, Rate +1%, Contribution +10%.

G) Heading: Notes and Assumptions

– State contribution timing (end vs. beginning of period) and how that changes totals.

– Clarify that taxes, fees, and inflation are excluded unless specified.

Rules

– Keep math consistent with the compounding formula.

– If any input is missing, ask one brief clarifying question, then proceed with a reasonable default and label it “Assumed.”

– Avoid giving investment advice; present informational math and general strategies only.

– Keep tables readable (no more than 12–15 columns wide).